Destruction of Your Money... and the Solution

Stories of the impacts of inflation and the solutions

I spoke with a very good friend this week and he wanted to better understand why I keep going on about Bitcoin?

Great question but as I explained to him - Bitcoin is the solution, first we need to start with the problem.

What Problem is Bitcoin Solving?

In my discussion, I started by asking my friend if he’s feeling the effects of inflation? Yes, of course…

I went on describe some personal stories of friends and family in my close circle and their struggles with inflation:

A friend sold their house years ago and has been renting and is now struggling to get back into the real estate market. House prices have far outpaced their savings…

Another friend is thinking of selling their house to downsize because it’s now becoming almost impossible to afford the house. The cost of housing has far outpaced their salary growth…

A retired friend needs to sell their house to use the money to fund their retirement. The amount they had put aside for retirement all of the sudden seems inadequate…

A friend wanted his spouse to stay home to raise their young family but, despite him having a great job and salary, found it impossible with the cost of life today and inflation…

A newlywed couple living in the Toronto Greater Golden Horseshoe area is finding it impossible to save up a downpayment to get their first house…

And for the five stories above, I know of many more. We all do. It’s a continual topic of conversation at virtually every event or party we go to. My friend and I concluded by agreeing:

Everyone today can feel that all scarce, desirable things like housing, quality food, energy, health care, education getting more and more expensive each day.

We are witnessing and living the effects of the destruction of our wages, savings and ultimately our money.

And it really pisses me off. Our kids are getting so screwed by what’s happening. Which is a huge motivator for me to write Bigger Things…

Okay, back to the story…

But No One Really Understands Why!

Why is this happening? Here it is explained in a single chart and 3 minute video by Nick at Rockstar Real Estate 🤯🤯…

From this you can see the rise in house prices from 1971 to now (another interesting resource - WTF Happened in 1971!?).

And then the rise, or lack there of, of income growth in comparison.

All of which results in the destruction of your savings and the DESTRUCTION OF THE MIDDLE CLASS, as Nick puts it.

So what can we do to protect ourselves from the destruction?

Why Owning Real Estate is (part of) the Solution

I started out by saying Bitcoin is the solution. But Real Estate is also part of the solution and is frankly easier to understand, so I’ll start with that.

In the last few month we’ve had to replace a roof, deal with two sewer backups into a basement, deal with tenant non-payment of rent. Real estate is not without its challenges but despite all that, I still believe in it and love it. Why?

Because it provides one of the best and most easily understood way to hedge against currency debasement.

What do I mean?

In Canada over the past 24 years, average home prices are up 421%. 🤯🤯

Wow! What’s causing that? Let’s look at the amount of money in circulation in the Canada (known as M2), compiled below:

While house prices increased 421% over 24 years, the amount of money in circulation increased by 481% over the same period.

As Nick points out, the home price increases are correlated to the M2 money printing.

So did the price of the house really go up or did the value of the dollar decline?

When I say money in circulation in Canada, known as M2, went from $476 Billion to $2.49 Trillion it seems a little abstract. Let me say it another way.

For every $1 in circulation in Canada in 2000, there are now $4.81 in circulation in 2024.

Where did the extra $3.81 come from?

It was printed out of thin air, through new debt creation which the government now needs to pay interest on.

The effect of so many more dollars being printed is that more dollars are now chasing the same number of scarce assets.

This is why anything with scarcity including real estate, gold, a Picasso, a Rolex, collectibles, Bitcoin, the Magnificent 7 Stocks, all saw massive price increases during this time frame.

Let’s explain yet another way.

Imagine you had $163,000 in cash savings in the year 2000, it would have bought you an entire (average) house!

But instead of buying a house with it you held that $163,000 in cash.

Now 24 years later, that $163,000 would buy you a quarter of one house!

Savers have been getting punished!

That is why people need to save in something that has scarcity and for most, real estate is the best and simplest way.

Average house prices in the UK from the year 2000 to now went up 272% and M2 went up 233%… see the trend. Same correlation is true for the USA numbers.

This system we live in is so unfair. The money printing is the actual cause of the “haves” and “have nots”. Money printing is the actual cause of the destruction of your savings and destruction of the middle class.

Why Owning Bitcoin is (part of) the Solution

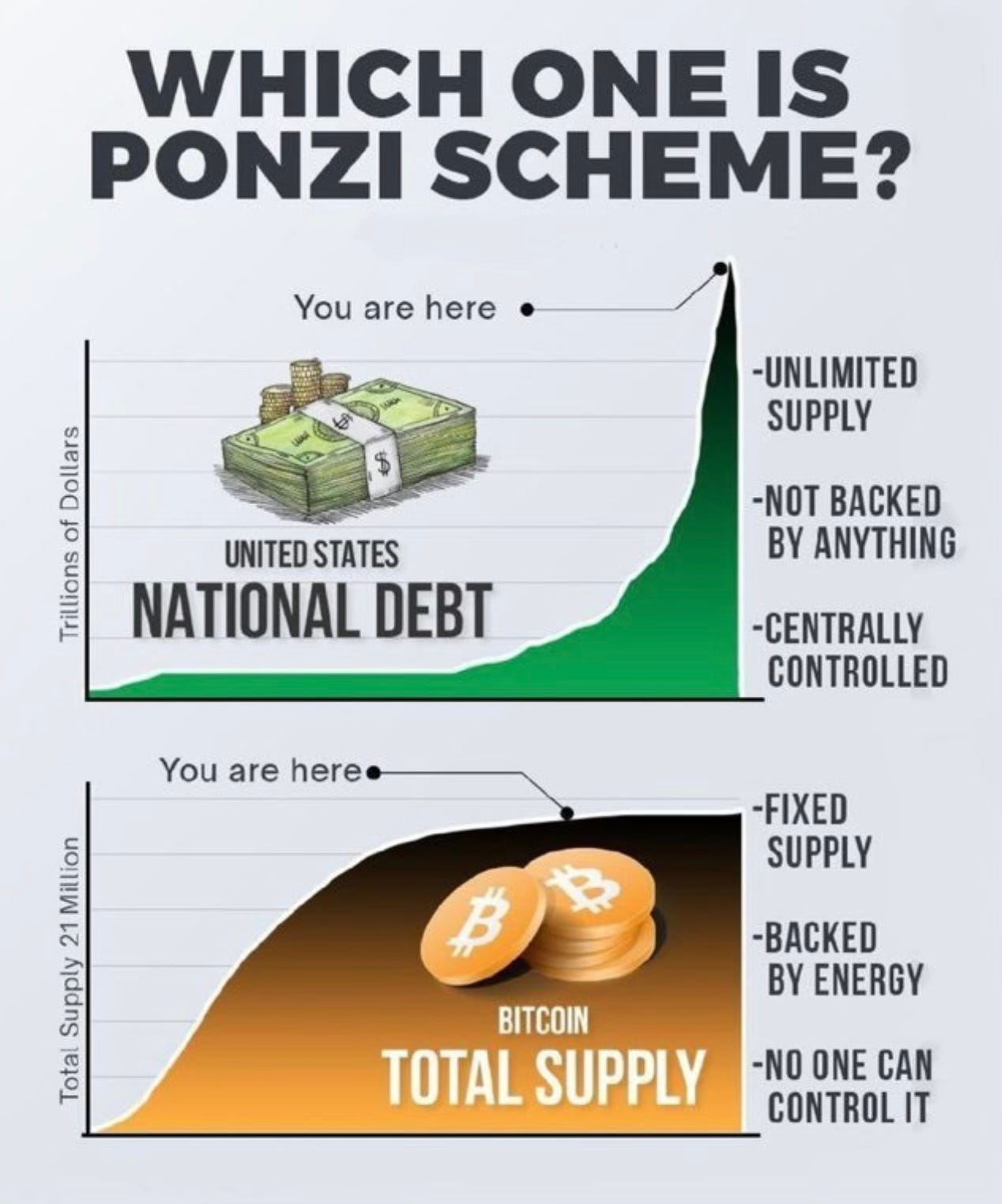

Someone asked me recently “at what point do I sell my real estate, surely prices on these houses can’t keep going up forever?”.

Actually they can.

It just depends on what you are measuring the price in. When measured in fiat, prices will go up forever.

REAL ESTATE PRICES HAVE NO TOP because the MONEY PRINTING HAS NO TOP and THE M2 DEBT SPIRAL HAS NO BOTTOM which means FIAT CURRENCY DEVALUATION HAS NO BOTTOM.

What happens if we measure the price of a home in something other than dollars? What if we measure the price in Bitcoin?

When measured in Bitcoin instead of dollars, the price of real estate is going down. DRAMATICALLY.

In 2016 the price of an average house in the USA cost 664 Bitcoin, today it only costs ~7 Bitcoin.

Satoshi Created the Most Beautiful Solution

On July 5, 2024 (two days ago), Bitcoin historian Pete Rizzo posted a quote from Satoshi from July 5, 2010…

"Bitcoin uses cryptography and a distributed network to replace the need for a trusted central server. Escape the arbitrary inflation risk of centrally managed currencies. Bitcoin's total circulation is limited to 21 million coins." - Satoshi Nakamoto on July 5, 2010 when the price of Bitcoin was $0.01

Rizzo commented “Satoshi Nakamoto on Bitcoin, exactly 14 years ago. True at $0.01, true today.” Today the price of one Bitcoin is around $57,000 USD.

Not only did Satoshi understand the issue of “arbitrary inflation risk” from “centrally managed currencies” - money printing - he/she/they engineered the most amazing, pristine and beautiful solution.

Satoshi literally built Bitcoin to help us escape the arbitrary inflation risk of centrally managed currencies.

Thank you Satoshi!

And so how do you protect yourself and your family from the destruction of your savings and the effects of inflation?

How do you get off the sinking ship of a debasing currency?

You need a “life boat”.

The life boat must be based on something that can't be easy created or replicated, something that has scarcity.

The more difficult to create or replicate the more valuable the life boat.

We need to own hard, scarce assets that cannot be printed out of thin air.

For me and my family, the “life boat” is Real Estate and Bitcoin. I hope this is helpful to you choosing yours.

One last detail, while it’s better to buy actual Bitcoin through an exchange like Bull Bitcoin or Swan Bitcoin, a lot of us have money tied up in registered accounts like RRSPs, RESPs, TFSAs in 🇨🇦 and 401Ks in 🇺🇸. You can buy Bitcoin ETFs in those registered accounts through most stock trading accounts.

To Your Bigger Things!

Brad 💕👊

You are receiving The Bigger Things Letter because you either signed up or you attended one of the events that I spoke at. Feel free to unsubscribe if you aren’t finding this valuable. Nothing in this email is intended to serve as financial advice. Do your own research.

You have a gift for distilling things down—this was a great read! Bitcoin for the win (again).

For those interested in gaining Bitcoin exposure through their brokerage account: Bitwise (BITB) may not be the biggest name on the list, but as of now, they are the only ones committing part of their proceeds (10%) to fund open-source developers working on and building out the Bitcoin protocol.